From Ti22’s vantage point inside procurement reviews and supply-chain turnarounds, rare earth elements (REEs) present a persistent strategic challenge: by the time a board recognises that dependence on a single jurisdiction is unsustainable, the industrial calendar has already run its course. Mines, separation plants, alloy and magnet lines, and the qualification pipelines above them move on 24- to 36-month cycles, not quarterly sourcing timelines.

Key Takeaways

REE supply chains require 24–36 months from investment decision to on-spec material, driven by permitting, construction and qualification.

Regulatory shifts—Chinese export controls and Western environmental permits—operate on political timescales that often misalign with industrial build-outs.

Downstream sectors such as defence, EV powertrains and aerospace add qualification cycles that can exceed a year for material changes.

Temporary “policy pauses” may not be long enough to bring non-Chinese capacity fully online before controls resume.

Rare earth sourcing now resembles strategic capacity planning, with implications for contracting horizons, inventory policy and supplier selection.

1. Structure of the Rare Earth Supply Chain

Rare earth elements (REEs) are relatively abundant geologically; the bottleneck lies in processing and downstream transformation. The chain typically comprises five stages:

Mining and concentration: extraction of ore and production of mineral concentrates.

Chemical separation: hydrometallurgical circuits that yield individual high-purity oxides; capital- and permit-intensive.

Metal and alloy making: conversion of oxides into metals and magnet alloys (e.g., NdFeB).

Component fabrication: manufacture of magnets and other REE-based components.

End-use integration: incorporation into motors, generators, sensors or catalysts across defence, EV, wind and electronics sectors.

As of 2024, mining occurs in China, the U.S., Australia and parts of Africa, but separation and magnet-making capacity remain heavily concentrated in China. Non-Chinese processing exists at smaller scale and with narrower product ranges, meaning switching a mine often implies building or qualifying new separation and magnet capacity under stricter environmental and safety regimes.

2. Regulatory Frameworks and Export Controls

Multiple overlapping regulations shape REE flows across borders and into sensitive applications:

China’s Export Control Law (ECL): Since 2020, the ECL underpins licensing for sensitive items, with recent extensions to gallium, germanium and select graphite.

Industrial catalogues and quotas: China uses production quotas and environmental standards to steer REE output and exports.

U.S. Defense Production Act (DPA): Grants, loans and offtake commitments to underwrite non-Chinese separation and magnet projects on national security grounds.

EU Critical Raw Materials Act: Targets domestic extraction, processing and recycling, and streamlines permitting for strategic projects.

Defence procurement rules: ITAR, DFARS and international equivalents impose sourcing and traceability requirements on REE components.

Even if a new facility secures basic operating permits, it may still fail to meet defence or export-control traceability standards for certain end-uses, adding further lead time.

3. Permitting, Construction and Commissioning Timelines

From final investment decision to first on-spec production, complex chemical and metallurgical plants face multi-year timelines:

Environmental impact assessments: NEPA- or EPBC-type reviews, public consultations and radiation safety plans.

Water and waste permits: Community challenges around contamination risks.

Health and safety approvals: Handling hazardous reagents in separation circuits.

Land access and indigenous rights: Multi-year negotiation and consent processes.

Concrete curing, equipment delivery and regulatory inspections are calendar-bound. Even with premium project management, solvent-extraction commissioning and consistent product specification iterations demand time.

4. Qualification and Compliance in Downstream Sectors

Defence, aerospace and automotive sectors impose rigorous qualification campaigns for any material or supplier change:

Defence and aerospace: Mechanical, thermal, vibration and reliability tests, sometimes including flight trials, spanning multiple budget cycles.

Automotive and EV: Advanced Product Quality Planning (APQP), Production Part Approval Process (PPAP), NVH and durability testing, commonly lasting several months.

Electronics and optics: Extended burn-in, thermal cycling and humidity tests for phosphors, lasers or optical components.

Compliance overlays—non-Chinese content verification, embargo-free processing—extend acceptance timelines. In Ti22 audits, pure testing for a new magnet supplier has consumed a year or more.

5. Historical Supply Shocks

Past disruptions illustrate the inertia:

2010 China–Japan dispute: Japan’s export slowdowns triggered stockpiling and alternative project funding, yet meaningful diversification took years.

2019–2020 U.S.–China trade tensions: Rhetoric on REE restrictions led to contingency plans that proved unrealistic within a single year.

2023 gallium and germanium controls: Licensing requirements spurred interest in new sources, but industry reporting confirmed multi-year lead times to scale alternatives.

Interpretation: The 24-Month Problem as a Strategic Imperative

We at Ti22 observe that today’s policy headlines—whether “truces” in export controls or fresh incentives for non-Chinese capacity—rarely align with industrial build-out. Supply reconfiguration for REEs is a multi-year endeavour, not a tactical quarter-end fix. Boards must treat REE sourcing as strategic capacity planning, revisiting contracting horizons, inventory norms and supplier diversification well in advance of anticipated controls or demand shifts.

Conclusion

Rare earth supply chains are inherently slow to reconfigure due to permitting, construction and downstream qualification phases that span 24–36 months. Temporary regulatory reliefs or stockpile strategies offer limited respite if non-Chinese processing capacity cannot come online before controls resume. Companies should align board-level risk appetite with realistic project timelines and reframe REE sourcing as a long-term industrial capacity issue rather than a short-term commodity purchase.

Executive summary:Graphite is the least visible but most structurally fragile node in the EV battery chain: up to 99% of anode volume, with more than 90% of spherical graphite capacity concentrated in China and less than 5% of global active anode material capacity outside China. Recent Chinese export controls, emerging Foreign Entity of Concern (FEOC) rules and qualification setbacks at flagship Western projects such as Syrah’s Vidalia plant demonstrate that the constraint is now midstream process control, permitting and geopolitics as much as geology. Mapping 12 strategically critical projects across North America, Africa and emerging hubs in the Andes and Arctic shows a narrow 2024–2028 window in which a handful of technically complex plants will determine whether Western supply chains gain a resilient graphite base or remain exposed to a single midstream jurisdiction.

Key takeaways

Graphite (in battery use, referred to here as active anode material or AAM) can represent up to 99% of anode volume by material, but processing—purification, spheronization and coating—is the bottleneck.

China dominates midstream processing and spherical-graphite capacity; export quota adjustments and MOFCOM policy shifts since 2023 have tightened external supply.

Western policy layers (e.g., the U.S. Inflation Reduction Act and FEOC screening) raise technical and compliance barriers for ex-China projects, putting near-term projects under intense scrutiny.

A small cluster of plants (notably Vidalia) will determine whether allied EV chains can secure qualified AAM capacity by the mid-decade.

Graphite: the supply-side paradox

Graphite’s geological abundance masks a classic single-point failure in the value chain. Mining and flake production have diversified geographically at the margins, but the conversion of flake to battery-grade coated spherical graphite—the active anode material (AAM)—is highly technical and remains heavily concentrated in China. The Ministry of Commerce of the People’s Republic of China (MOFCOM) has tightened export controls on certain graphite products in recent years; those measures, together with quota adjustments introduced from January 2025, have reduced licensed battery-grade exports and lengthened lead times for buyers outside China, according to industry reporting.

What battery‑grade graphite entails

Battery-grade AAM is not a commodity lump: it requires a sequence of narrow, high-control operations. At first use in this piece, we define FEOC as Foreign Entity of Concern—policy measures that restrict engagement with suppliers, technology or ownership structures linked to certain jurisdictions. Other policy levers referenced here include the U.S. Inflation Reduction Act (IRA) and the EU’s Carbon Border Adjustment Mechanism (CBAM), which add content and carbon-intensity constraints to subsidy eligibility.

From ore to flake concentrate

Most natural graphite origins are open-pit or underground operations extracting graphitic schist or gneiss. Ore is crushed and floated to produce flake concentrates typically in the 94–97% total graphitic carbon (Cg) range. Flake-size distribution matters: superfine feedstocks are better suited to spheroidization for EV anodes, while jumbo flakes are valuable in refractories but require additional processing to become AAM. Several non-Chinese projects now produce concentrates designed with battery markets in mind, but producing concentrate is only one link in a longer chain.

Purification, spheronization and coating

Transforming flake concentrate into EV-grade AAM exposes the chokepoint. Typical EV anodes demand carbon purities above 99.9%–99.95%, controlled particle-size distributions (often sub-15 micron target sizes in some cell designs), and extremely low metallic and sulfur impurities. Achieving those parameters involves highly coupled unit operations: chemical or thermal purification (acid leach or high-temperature graphitization), jet milling and spheronization to create spherical particles, and surface treatment/coating to tailor first-cycle loss and long-term SEI behaviour. Each stage drives capital and operating costs—reactor design, acid recovery, energy needs and waste treatment are all gating factors—and small deviations in process control can cause product disqualification at cell manufacturers.

The qualification difficulties at large Western demonstration plants underline this risk. Producing laboratory-scale material is a different engineering problem from delivering consistent, commercial-quality AAM at throughput. Qualification failures typically trace back to coupled issues such as impurity removal efficiency, particle-size distribution control and electrochemical stability—parameters that are sensitive to reactor residence times, acid recovery and neutralization protocols, milling energy regimes and coating uniformity.

Natural, synthetic and hybrid routes

Natural graphite routes can offer lower embedded emissions compared with synthetic graphite (the latter derives from petroleum or needle coke and requires energy‑intensive high‑temperature graphitization). Synthetic routes do, however, provide highly predictable purity and morphology, which is why some high-performance cells have relied on them. Hybrid flowsheets—combining natural and synthetic processing stages—are being trialled by Western developers to hedge feedstock and qualification risk, but they add complexity to process control and qualification pathways.

China’s midstream dominance and the policy shock

Multiple industry trackers show that a large share of global spherical-graphite and purification capacity is located in China. As a result, mine-level diversification often funnels concentrates back to China for the highest‑value transformation steps. Since late 2023, export management changes and quota tightening by MOFCOM have reduced available licensed exports of battery-grade graphite, pushing spot prices higher and extending order-to-delivery timelines for buyers reliant on Chinese coated spherical graphite. That shock has come concurrently with Western policy incentives that penalize supply chains with links to FEOC jurisdictions or that fail to meet domestic-content rules—raising the bar for ex‑China projects to win offtakes and subsidies.

Near‑term strategic projects: why a few plants matter

A small set of projects—selected for their strategic location, feedstock security and claimed processing capabilities—sits at the intersection of supply deficit, qualification risk and policy scrutiny. If these plants fail to qualify material or to ramp reliably, allied EV supply chains will face constrained AAM access and extended reliance on Chinese midstream capacity.

Syrah Resources’ Vidalia AAM facility (Louisiana, USA)

Vidalia is the flagship Western attempt to build a vertically integrated, large‑scale AAM producer. Phase 1 is designed for roughly 11,250 tonnes per year of AAM with a planned ramp to higher nameplate levels, and an offtake arrangement with an EV OEM is part of the commercial underpinning. Feedstock from the Balama mine in Mozambique gives Syrah an end‑to‑end supply chain in principle. But in practice, the plant has faced repeated challenges meeting EV‑grade electrochemical and purity specifications on a consistent basis, prompting successive cure periods under the supply contract and extensions while technical and financing discussions continue with stakeholders and the U.S. Department of Energy. These developments illustrate the dual technical and commercial risk of converting flake into qualified AAM at scale in a Western jurisdiction.

Implications for market participants

Procurers, OEMs and policy designers should treat AAM as a midstream risk more than a raw-material one. Near-term resilience depends on: (1) accelerating robust qualification pipelines and independent electrochemical testing; (2) prioritizing projects that demonstrate repeatable process control and waste‑management systems; and (3) designing subsidy and offtake terms that recognise extended commissioning and qualification timelines without distorting incentives for rigorous process development.

Conclusion

Graphite is a strategic chokepoint because the midstream, not the mine, concentrates technical risk and geopolitical leverage. The 2024–2028 horizon is decisive: a small number of technically complex plants will determine whether Western EV chains can secure trusted, qualified AAM capacity. Market actors should align procurement, technical qualification and policy engagement to avoid a midstream single‑point failure repeating across the EV value chain.

Antimony has never been the headline metal in most sourcing reviews run or audited over the last decade. Yet, in practice, it has repeatedly behaved like one of the most strategic levers in flame retardant systems, PET packaging chains, and legacy energy storage. The reason this matters is simple: risk, continuity of supply, and regulatory exposure tend to concentrate on a few “boring” intermediates, and antimony has been one of them.

Several operational incidents pushed antimony onto the front row. A first shock came with sudden production disruptions at key Chinese smelters in the early 2010s, which translated into lead times slipping and contracts being reopened at short notice. A second inflection point was the wave of regulatory and ESG scrutiny on flame retardants and PET catalysts between 2015 and 2022, where internal risk committees started to ask why so much performance hinged on a single critical element with geographically concentrated supply.

Since then, every time a government announces new export controls on a critical input-gallium, germanium, rare earth magnets-the question resurfaces internally: what happens if antimony is next? The current briefing builds from that recurring board-level question, against a backdrop of high standards on security of supply, cost discipline, and compliance. The focus is narrow: definitions, current regulatory footing, potential export control architectures, and how these would flow through operations and supply chains.

Key takeaways (executive summary)

Antimony is already treated as a strategic material in multiple jurisdictions, but as of early 2024 there is no globally publicised, antimony-specific export control regime comparable to those on gallium or advanced semiconductors.

Industrial usage is heavily skewed: sectoral data indicate that flame retardants account for around 55% of global antimony consumption, and antimony catalysts are used in the vast majority of PET production, which concentrates regulatory and supply risk.

Most current policy interventions around antimony are indirect (critical raw material lists, environmental enforcement, stockpiling) rather than explicit export bans or licensing schemes, and several important parameters such as November 2025 measures are not specified in the elements provided.

If targeted export controls emerge, they are likely to hit hardest at antimony trioxide for flame retardants and catalyst-grade antimony compounds, with knock-on effects into electronics, textiles, packaging, and defense-linked alloys.

The main operational challenge is traceability and technical requalification: mapping where antimony truly sits in formulations and components has proven slower and more complex than many governance frameworks initially assumed.

FACTS: Current knowledge on antimony, regulation and supply

Industrial role and concentration of use

Available sectoral data and the sources cited in the initial request converge on a few key points regarding industrial usage of antimony:

Flame retardants: Approximately 55% of global antimony consumption is associated with flame retardant systems, especially antimony trioxide used as a synergist with halogenated flame retardants in plastics, electronics housings, textiles, upholstery, and building materials.

PET and synthetic fibers: Antimony catalysts are used in the production of polyethylene terephthalate (PET). The data provided indicate that around 90% of global PET production relies on antimony-based catalysts, notably for beverage bottles and synthetic fibers.

Alloys and energy storage: Antimony is a long-standing alloying element in lead-acid batteries, ammunition, solders, bearings, and cable sheathing, supporting both civilian and defense-linked applications.

Semiconductors and infrared optics: Antimony compounds such as indium antimonide are used in niche but technologically critical applications including infrared detectors and certain semiconductor devices.

This sectoral concentration is not an interpretation; it is a structural feature of current industrial practice. It is also one of the reasons antimony appears on multiple national and regional lists of critical raw materials or strategic minerals, even when public debate remains relatively muted compared to lithium, cobalt, or rare earths.

Critical raw material status and strategic framing

As of early 2024, antimony features on several critical raw material or strategic mineral lists. These lists differ in methodology, but generally emphasise supply concentration, economic importance, and substitution difficulty. Examples include:

United States: Antimony is included in the U.S. Geological Survey’s list of critical minerals. Historically, it has also been part of the National Defense Stockpile portfolio managed by the Defense Logistics Agency, reflecting perceived defense relevance.

European Union: Antimony appears on the EU’s Critical Raw Materials list, which informs monitoring, strategic projects, and potential policy responses. Inclusion does not automatically trigger export controls but formalises the “criticality” label in EU policy language.

Other jurisdictions: Several countries with advanced manufacturing or defense sectors reference antimony in national critical minerals strategies or risk assessments, although the level of public detail varies and is not fully captured in the elements provided.

Inclusion on these lists is a factual policy signal: antimony is officially recognised as strategically important in multiple major economies. that said, criticality designation is distinct from export control status.

Export controls: current public footing (pre‑2024)

Export controls can target materials directly, or indirectly via finished products and dual-use technologies. Antimony’s current status, based on public information available up to early 2024, can be summarised as follows:

No widely publicised, antimony-specific global export control regime: Unlike gallium, germanium, or advanced semiconductor items, antimony metal as a bulk commodity does not appear as a headline item in major export control updates publicly communicated by key jurisdictions up to early 2024.

Dual-use and defense categories: Certain antimony-containing products (for example, specific munitions, infrared detection systems, or specialized electronics) may fall under munitions lists or dual-use export controls. In those cases, antimony is embedded within a controlled system rather than being the explicit subject of the control.

Producer-country licensing frameworks: Major producing countries operate general export licensing and customs regimes that apply to a broad range of minerals and metals, including antimony. These frameworks can, in practice, slow or condition exports without being described internationally as “export bans” or high-profile controls.

Crucially, the materials provided for this briefing do not specify any concrete antimony export control text, regulatory reference, or November 2025 suspension decision. Where such measures exist or are being developed, they are not described in the input and thus cannot be characterised in detail here without speculation.

China’s role and known policy levers

Public geological and mining data, as well as long-running market practice, show that antimony supply is heavily concentrated, with China historically playing a dominant role in mining and smelting. Other important jurisdictions include parts of Central Asia, Russia, and certain smaller producers, but the supply stack is far from diversified.

Chinese authorities have a long track record of managing resource sectors through a mix of tools: production quotas, environmental inspections, export licensing requirements, and consolidation policies. Antimony has been affected by some of these measures over the years, particularly on the production and environmental side. However, based on widely reported policy updates up to early 2024, antimony has not been placed under the same type of high-visibility, targeted export controls that were applied to other materials such as gallium and germanium.

This distinction matters: production-side discipline and environmental enforcement can tighten export availability and raise concerns in supply chain planning, but they are structurally different from a formal export control designation explicitly naming antimony as a restricted strategic material.

Data gaps and non‑specified elements

A number of aspects requested in the initial research brief are not documented in the materials provided and are not reliably inferable from general industrial data alone. These include:

Any explicit November 2025 export suspension or control decision affecting antimony.

Current and projected mining, refining, and export capacity by jurisdiction, beyond the qualitative recognition that supply is geographically concentrated.

Operational status of individual mines or smelters and the precise impact of local environmental or safety enforcement actions.

Detailed compliance frameworks specific to antimony in customs codes or export licensing catalogues, beyond generic mineral export regulations.

Quantified supply chain concentration metrics and market pricing data for antimony and its compounds.

These gaps are factual constraints. They do not prevent scenario analysis, but they do limit the precision with which any specific regulatory timeline or market outcome can be described.

How antimony export controls could play out operationally

From an operational and governance standpoint, antimony sits in a risk category that has repeatedly surprised executive teams: technically “minor” by volume or value in many bills of materials, but systemically important due to performance roles and substitution difficulty. Over multiple procurement cycles, that pattern has encouraged treating antimony more like a strategic choke point than a simple commodity input.

Why antimony is a natural candidate in export control debates

There are structural reasons why antimony appears regularly in internal scenario discussions about future export controls, even in the absence of a formal regime today:

Defense relevance: Antimony-bearing alloys are present in ammunition and legacy energy storage, and antimony compounds are embedded in certain infrared detection and guidance systems. This creates a bridge into national security discussions.

Consumer safety and standards: Flame retardancy in electronics, vehicles, and buildings is a critical safety function. Regulators and manufacturers are reluctant to compromise performance, which makes antimony trioxide difficult to replace at scale.

Supply concentration: Heavy reliance on a single or small group of producing countries has repeatedly translated into supply vulnerability for other critical materials. Antimony fits that pattern.

Low public profile: Compared with high-profile energy transition metals, antimony attracts less public scrutiny. This can make it more tempting for policymakers to use it as a low-visibility lever within broader trade or security strategies.

These elements are not predictions, but they explain why antimony is often included in internal export control war-gaming exercises alongside better-known strategic inputs.

Possible architectures of antimony export controls

If a jurisdiction were to introduce targeted export controls on antimony, several design options are plausible based on patterns seen in other sectors. Each has distinct implications for supply chains.

Material-level licensing: Export of antimony metal, antimony trioxide, and selected antimony compounds could be placed under a licensing regime. In practice, this would introduce case-by-case approval, varying lead times, and the possibility of destination-specific restrictions. From experience with other licensed materials, the operational impact tends to appear first in uncertainty and planning buffers rather than in outright bans.

End-use or end-user controls: Controls could focus on exports of antimony-containing materials to specific sectors (for example, defense, advanced sensing) or to specific entities. Here, downstream buyers in sensitive sectors might face additional documentation and due diligence steps, even if bulk commodity trade continues relatively smoothly.

Quota-based systems: A jurisdiction could authorise only a certain volume of antimony exports per period, allocated through licenses or state trading entities. For buyers used to relatively fungible supply, this scenario resembles the quota management seen in some fertilizer and energy markets.

Indirect leverage via environmental and safety rules: Stricter enforcement on mining and smelting, or reclassification of antimony compounds under occupational or environmental regulations, can tighten effective export availability without being labelled formally as “export controls”. This pathway has already been visible in other sectors and is consistent with prior experience in antimony and related minerals.

Which architecture a government might choose would depend heavily on its policy goals: revenue, strategic leverage, environmental performance, or a combination. The key point from a supply chain angle is that even a modest licensing requirement can reframe antimony from a bulk chemical to a “governed” input with longer and more variable lead times.

Operational transmission mechanisms into supply chains

In day-to-day purchasing and manufacturing, export controls rarely show up as a clean legal change and nothing else. Instead, they propagate through a series of familiar bottlenecks that have been observed repeatedly in other controlled materials:

Traceability and specification clarity: In multiple audits of flame retardant and PET supply chains, antimony often appeared as a sub-component in masterbatches, catalysts, or “black box” additive packages, with incomplete visibility at OEM or brand level. Any move toward export controls would increase the importance of knowing exactly which formulations contain antimony, in what form, and from which smelters.

Certification and requalification timelines: Changing flame retardant systems or PET catalysts has historically required extensive testing, certification, and sometimes retooling. In sectors such as automotive or building materials, those cycles can span several years. Export controls that tighten supply faster than requalification cycles proceed can generate hard bottlenecks.

Contractual rigidity vs. regulatory flexibility: Long-term supply agreements often assume relatively stable freedom to source globally. In past episodes involving other materials, export licensing or quota changes outpaced contract adjustment mechanisms, putting legal and operational teams under pressure to reconcile obligations with new regulatory constraints.

Risk cascades into adjacent materials: If antimony becomes constrained, demand can shift toward alternative flame retardant chemistries or catalysts. Prior experience suggests that this can stress supply chains for substitutes, especially where industrial capacity or regulatory acceptance is limited.

Over the last decade, several organisations learned these lessons the hard way through environmental reclassifications and regional production disruptions, even without formal export bans. Those episodes are a useful analogue for thinking through antimony risk under a prospective export control regime.

Trade-offs: security objectives vs. systemic risk

Any serious reading of prospective antimony export controls has to acknowledge the core trade-off: measures intended to enhance national security or bargaining power can introduce systemic safety and reliability risks elsewhere.

Fire safety and building codes: Flame retardants enabled by antimony trioxide underpin compliance with fire standards in electronics, transport, and construction. Aggressive constraints on supply, without validated alternatives, could force difficult choices between safety performance, cost, and design complexity.

Legacy systems and maintenance: Defense platforms, grid infrastructure, and industrial equipment built around antimony-containing alloys or batteries are not easily redesigned mid‑life. Export controls that disrupt availability of replacement components or materials can have long-lived effects on fleet readiness and reliability.

Regulatory alignment: Export controls imposed by one jurisdiction can clash with safety, environmental, or product standards in others. The resulting friction tends to land on procurement and compliance teams, which must reconcile conflicting regulatory signals.

Geopolitical signalling vs. supply chain stability: Using antimony as a geopolitical lever may deliver short-term signalling value but could accelerate diversification and stockpiling efforts among importing regions, reshaping long-term demand patterns. How that balance plays out would depend on the specific design and duration of any controls.

In prior commodity cycles, underestimation of these trade-offs led to abrupt strategy reversals once downstream impacts became clearer. Antimony would not be an exception; the same structural dynamics would apply.

WHAT TO WATCH: Signals and indicators around antimony

Given the current absence of clearly specified, high-profile antimony export controls in the public record up to early 2024, forward-looking monitoring becomes central. Several classes of signals stand out as particularly informative:

Official export control catalogues and customs lists: Any explicit addition of antimony metal, antimony trioxide, or key antimony compounds to export control lists or licensing catalogues in major producing countries would be a clear inflection point.

Critical mineral policy updates: Changes in how the United States, European Union, Japan, or other industrial powers classify antimony-especially if linked to stockpiling, defense procurement, or industrial policy—would refine the strategic framing even if they stop short of export bans.

Environmental and health reclassifications: New toxicological assessments or occupational exposure limits for antimony compounds could drive regulatory action indirectly, including tighter control of production and, by extension, exports.

State stockpile behaviour: Accelerated government purchases, tenders, or disposals of antimony for strategic reserves, where publicly disclosed, can signal shifting policy priorities and expectations about future availability.

Corporate disclosures: References to antimony as a “critical” or “at risk” input in annual reports, sustainability disclosures, or risk registers from large manufacturers can reveal emerging concerns before they translate into public regulation.

Innovation and substitution efforts: Increased R&D spending on antimony-free flame retardants or alternative PET catalysts, and announcements of commercial-scale adoption, would indicate that industrial actors anticipate possible regulatory or supply constraints.

Trade flow anomalies: Sudden, unexplained shifts in reported antimony exports or imports by key jurisdictions—where data are available—can sometimes prefigure the formalisation of new policy constraints.

None of these signals alone confirms the emergence of a binding export control regime. Together, however, they provide a structured set of indicators for tracking how antimony moves up or down the strategic priority list of governments and large industrial actors.

Conclusion

Antimony sits in an uncomfortable but familiar position: officially recognised as a critical raw material in multiple jurisdictions, heavily embedded in safety-critical and defense-relevant applications, and supplied from a geographically concentrated base, yet not (as of early 2024) subject to highly public antimony-specific export control regimes. That disconnect is precisely what keeps the topic alive in risk committees and board discussions.

The facts available support a clear message: antimony’s strategic weight comes less from overall tonnage and more from its role as a performance enabler in flame retardants, PET, alloys, and advanced sensing. Export controls, if and when they materialise, are likely to propagate through traceability, certification, and regulatory alignment challenges rather than as a single, visible legal switch.

In the absence of detailed public texts on measures such as an alleged November 2025 suspension, rigorous analysis has to stay grounded in what is documented, while using experience from other controlled materials to outline plausible operational trajectories. Under those constraints, the most robust position is to treat antimony as a structurally strategic input whose regulatory and supply risks are still in flux, warranting active monitoring of weak signals across both policy and industry behaviour.

Note on the TI22 methodology This briefing draws on a systematic reading of publicly available regulatory texts and official communications from relevant authorities, cross-checked against the industrial concentration and usage patterns described in the initial request. Where market evidence is available, it is used qualitatively rather than to infer precise pricing or capacity figures, and is combined with technical analysis of end-use specifications in flame retardants, PET, alloys, and semiconductor applications to understand how regulatory shifts could translate into operational constraints.

**China’s 2025 rare earth export controls represent a structural shift: from tonnage-based trade measures to a fine‑grained regime combining material, technology, and extraterritorial rules. The 0.1% de minimis threshold, mandatory compliance notifications, and controls on mining and processing know‑how rewire how rare earths, magnets, and battery materials move through global supply chains. The temporary suspension of part of the regime until 10 November 2026 does not unwind the architecture; it simply creates a narrow window in which operational choices and technical configurations will determine who absorbs the next shock.**

China’s Rare Earth Export Controls: From Tariffs Response to Systemic Redesign (2025-2026)

The rare earth export controls deployed by China between April and November 2025 mark a decisive break from earlier commodity‑focused measures. What began as a direct response to U.S. tariffs rapidly evolved into a multi‑layered system covering specific rare earth elements (REE), production equipment, intangible technologies, and even foreign‑made products containing Chinese content above a 0.1% value threshold.

This architecture is more than a diplomatic signal. It inserts Chinese licensing authority deep into midstream and downstream industrial flows that rely on heavy and light rare earths, permanent magnets, and certain lithium‑ion battery materials. The temporary suspension of the second wave of measures until 10 November 2026 relieves short‑term pressure but leaves the underlying compliance and traceability regime firmly in place.

For technical decision‑makers in mining, separation, metallurgy, and advanced manufacturing, the controls reshape three core questions: which process technologies can be deployed outside China, which material routes remain licensable and predictable, and how far extraterritorial reach extends into complex multi‑tier supply chains. The sections below dissect the regulatory timeline, scope, compliance mechanics, and plausible 2026 trajectories through a technical and operational lens.

I. Regulatory Timeline: Three Restrictive Waves in Seven Months

1. First Wave – 4 April 2025: Announcement 18 and Initial Heavy Rare Earth Controls

On 4 April 2025, in direct reaction to the so‑called “Liberation Day” tariffs imposed by the U.S. administration, China’s Ministry of Commerce (MOFCOM) and the General Administration of Customs issued Announcement No. 18 of 2025. This first wave introduced export controls on seven heavy rare earth elements and their associated compounds, metals, and magnets [2]. Although the list in public summaries is not fully itemized, it clearly targets heavy REEs that are critical to high‑performance permanent magnets and defence‑relevant alloys.

From an operational standpoint, Announcement 18 did three things. It imposed licensing requirements on exports of the listed elements and associated products; it required detailed disclosure of end users and end uses; and it created an administrative gate through which sensitive applications could be filtered. Industry feedback described the licensing workflow as opaque and selectively enforced, with lead times that introduced new uncertainty into contract performance [2].

On 13 May 2025, China agreed to suspend these non‑tariff measures, including the rare earth restrictions, for 90 days as part of tariff negotiations with the United States [6]. The pause reduced immediate shipment risk but left the institutional machinery-licensing protocols, lists, and enforcement structures-intact, ready for redeployment.

2. Second Wave – 9 October 2025: Decrees 61 & 62 and a Step‑Change in Scope

The second wave, announced on 9 October 2025, transformed a targeted response into a systemic control regime. MOFCOM Decrees No. 61 and 62 of 2025 expanded export controls along three axes [1]: additional rare earth elements, upstream and midstream technologies, and foreign‑made products containing Chinese rare earth inputs.

Decree 61 focused on metals and products related to rare earths, including those manufactured outside China that incorporate Chinese‑origin materials. Decree 62 concentrated on associated technologies, spanning mining, smelting and separation, magnet materials, and recycling [1]. On the same day, four related measures imposed controls on [1]:

Certain rare earth manufacturing equipment and associated materials/components

Five rare earth minerals and related materials: holmium, erbium, thulium, europium, and ytterbium

Selected materials and components for lithium‑ion batteries and artificial graphite anodes

Categories of “super materials” and associated equipment

A fifth decision placed 14 firms on China’s Unreliable Entity List [1]. Together, these moves extended controls beyond tangible raw materials to encompass technological know‑how and the foreign plants that rely on it. The number of controlled rare earth elements increased by five, bringing the total to 12 across the first and second waves [2]. Parallel commentary noted that neodymium, dysprosium, terbium, samarium, and praseodymium were also referenced in new regulations entering into force on 1 December 2025 [4], signalling attention to the key magnet and phosphor elements used in EV drivetrains, wind turbines, and optics.

3. Third Wave – 7–8 November 2025: Temporary Suspension and Extraterritorial Reach

On 7 November 2025, the Chinese government announced a temporary suspension of the second‑wave export controls until 10 November 2026 [2][7]. The suspension covered Decrees 61 and 62 and associated extraterritorial provisions, while leaving the April measures in force. Market reaction treated this as a de‑escalation, but the relief was partial and conditional.

One day later, on 8 November 2025, MOFCOM and the General Administration of Customs issued Announcements 55–58 of 2025, effective immediately [3]. These announcements broadened control coverage to include:

Super materials and related equipment

Rare earth processing equipment

Raw rare earth materials

Medium and heavy rare earth products

Lithium‑ion battery materials and artificial graphite anodes

The structure of the regime therefore shifted, but was not dismantled. The suspension postponed full activation of the extraterritorial and technology‑transfer components while consolidating control over equipment, raw materials, and selected downstream products.

II. Scope of Control: 12 Rare Earths, Technology Layers, and the 0.1% Rule

1. The Controlled Rare Earth Elements

Across the first two waves, 12 rare earth elements moved into explicit Chinese export control coverage [2]. The five added on 9 October 2025-holmium, erbium, thulium, europium, and ytterbium—are all heavy or middle REEs with specialised roles in lasers, high‑end optics, phosphors, and magnet modifications [1]. Combined with the earlier group of seven heavy REEs and expanded mention of neodymium, dysprosium, terbium, samarium, and praseodymium in later regulations [4], the focus is clear: functional bottlenecks in permanent magnets, display technologies, and defence‑relevant components.

This is not a blanket restriction on all 17 rare earth elements. Instead, it targets those with the tightest Chinese dominance in mining and, more importantly, separation and metal‑making. That targeting is where technical leverage translates directly into regulatory leverage.

2. Extraterritoriality via the 0.1% Value Threshold

The most structurally novel element is the assertion of extraterritorial control through a de minimis‑style rule. If a foreign‑manufactured product contains Chinese‑origin rare earth materials whose value exceeds 0.1% of the value of an independently usable unit, subsequent export of that product to a third country can also require MOFCOM approval [3].

This 0.1% threshold is remarkably low compared with typical export control de minimis rules in other jurisdictions, which often operate at substantially higher value shares. It pulls a wide range of assemblies into scope: motors, drives, sensors, catalysts, and consumer electronics where rare earth magnets or phosphors constitute a small share of bill‑of‑materials cost but are functionally critical.

Operationally, this extraterritorial design converts Chinese origin status from a customs attribute into a compliance attribute that follows the product through successive transformations. Each time a motor or sub‑assembly crosses a border, the presence of controlled Chinese REE content can, in principle, trigger an additional licensing step if the final destination is a third market.

3. Controlled Technologies and Know‑How

Beyond materials, the second and third waves placed a range of rare earth–related technologies under export control [1][3][5]. These include:

Rare earth mining technologies, including certain advanced beneficiation and in‑situ leaching methods

Metal smelting and alloying relevant to REE‑based alloys and master alloys

Magnetic materials manufacturing technologies (notably for NdFeB and related magnet grades)

Recycling technologies for secondary rare earth resources

Assembly and maintenance of rare earth production lines

Controls on mining technologies took effect immediately, while others became effective on 8 November 2025 [5]. For non‑Chinese projects seeking to deploy Chinese‑designed solvent extraction circuits, magnet sintering lines, or separation processes, this creates a new layer of complexity. Technology transfer agreements, technical services, remote monitoring of plants, and even dispatch of maintenance engineers can all fall under the definition of controlled technology export.

4. Adjacent Materials: Lithium‑Ion Batteries, Graphite, and “Super Materials”

The second and third waves also captured selected materials and components used in lithium‑ion batteries and artificial graphite anodes, alongside undefined but clearly strategic “super materials” [1][3]. This placement is consistent with an integrated view of critical materials where rare earth magnets, battery chemistries, and advanced structural materials co‑evolve in electric vehicles, renewable generation, and defence platforms.

Technically, this bundling means that operational strategies designed around substituting away from rare earths into alternative technologies do not automatically escape Chinese export jurisdiction. A cathode material that avoids dysprosium might still rely on a controlled graphite anode; an electric motor that reduces neodymium content might still sit in a drivetrain whose battery materials are partially controlled.

III. Compliance Mechanics: Notification Chains and Traceability Load

1. Licensing: An Administrative Chokepoint

At the core of the regime sits the export licence. For the listed materials, technologies, and covered products, exporters must obtain a licence and submit detailed information on end users and end uses [2]. In practice, this transforms MOFCOM into an administrative chokepoint linking upstream mines and refiners, midstream processors, and downstream manufacturers across multiple jurisdictions.

Industry reporting describes the licensing process as non‑transparent and selectively enforced [2]. Processing times and approval criteria are not always published in full, and case‑by‑case discretion is significant. This creates a qualitative risk profile: applications associated with dual‑use (civil/military) potential or sensitive geographies face a higher probability of delay or denial [4], even when nominal product specifications are identical to those destined for lower‑risk markets.

2. Notification of Compliance Letters and Documentation Chains

To operationalise rare earth export regulations, MOFCOM introduced a mandatory “Notification of Compliance” system [1][3]. Each exporter or supplier of listed materials must provide a standardised declaration to the next entity in the chain, indicating:

That the shipment contains Chinese‑origin controlled materials

The share and nature of this controlled content

That re‑export of products made from this material may require a Chinese export licence

The initial Chinese exporter and subsequent foreign exporters are both expected to issue a MOFCOM‑format notification letter to their customers and ultimate users [1]. Downstream recipients are required to retain these records and pass the information forward [3], creating a documentation chain designed to map controlled content through multiple processing stages.

In a simple linear chain—mine, refiner, magnet producer, motor assembler—this is administratively manageable. In modern electronics and vehicle platforms with tier‑1, tier‑2, and tier‑3 suppliers across different continents, the notification system becomes significantly more complex. Rare earth‑containing modules can pass through several hands before integration into a finished product, each step generating obligations to track and transmit compliance status.

3. Data Burden and the Multi‑Tier “Snowball” Effect

The 0.1% de minimis threshold amplifies the data burden. Many assemblies where rare earth content is economically small but functionally essential now sit above the threshold. To determine whether a finished product triggers Chinese licensing for re‑export, firms in the chain need visibility into:

Bill‑of‑materials composition at component and sub‑component levels

Country‑of‑origin data for each rare earth–bearing input

Value attribution for controlled content relative to total unit value

For complex equipment (industrial drives, aircraft systems, medical devices), this creates a “snowball” effect. Each additional tier of sub‑assemblies potentially adds another layer of compliance questions, and any missing origin information at a lower tier can propagate uncertainty upstream. In practice, this often pushes engineering and procurement teams to re‑evaluate supplier mapping, enterprise resource planning (ERP) data structures, and contract language around origin disclosure.

IV. Official Rationale and Strategic Context

1. Security Narrative: Preventing Military and “Sensitive” Use

MOFCOM framed the new measures under a security narrative. Officials cited instances where foreign entities allegedly transferred Chinese‑origin rare earth products, directly or post‑processing, to organisations and individuals involved in military and other sensitive domains [1][2]. Chinese law enforcement agencies also reported cases where foreign entities illegally obtained rare earth technologies from China, produced related items abroad, and supplied them into military and sensitive applications [1].

Within this narrative, the export controls and extraterritorial provisions are presented as tools to prevent circumvention and to “safeguard national security” [1]. The inclusion of technology controls, not only on equipment but on process know‑how and production line maintenance, is consistent with a view that intangible capabilities can be as strategically significant as physical materials.

2. Trade and Diplomatic Leverage

European research institutes and policy centres emphasise another dimension: leverage. With rare earths, magnets, and battery materials deeply embedded in digital, green, and defence value chains, control over their cross‑border flows provides bargaining power in wider trade and technology negotiations [4]. Analysts note that the 2025 measures may represent only the opening phase, with additional export restrictions in 2026 considered plausible, particularly calibrated to favour countries seen as “neutral” in the broader tech rivalry [4].

This dual framing—security enforcement combined with negotiational leverage—aligns with the observed sequencing. Initial controls respond to tariffs; subsequent waves layer in extraterritoriality and technology coverage, then partially suspend some elements while locking in new documentation and traceability norms. The structure is flexible enough to tighten or relax specific levers without rewriting the entire framework.

V. Impact Along the Rare Earth Value Chain

1. Upstream Mining and Concentrate Flows

At the mine and concentrate level, the immediate impact is nuanced. Several non‑Chinese mining projects already produce mixed rare earth concentrates or heavy rare earth–bearing ores. However, separation capacity—especially for heavy REEs such as dysprosium, terbium, and the newly listed holmium, erbium, thulium, europium, and ytterbium—remains heavily concentrated in China.

Controls on mining technologies that took effect immediately [5] intersect directly with upstream projects that rely on Chinese process design, reagents, or in‑situ leaching methods for ion‑adsorption clays. For projects intending to send concentrates to China for separation, the traditional model (export concentrate, pay tolling fee, re‑import separated oxides or metals) must now be understood through the lens of licensing risk, especially where final outputs target sensitive end users or jurisdictions.

2. Midstream Separation, Refining, and Alloying

The midstream is the real choke point. Separation of mixed rare earth concentrates into individual oxides remains dominated by Chinese plants using solvent extraction, ion exchange, and associated calcination and reduction technologies. Controls on smelting and separation technologies, as well as on assembly and maintenance of production lines [1][3], are designed precisely where China’s technical advantage is deepest.

For separation plants and alloying facilities outside China, several operational dependencies come into focus:

Design and optimisation of solvent extraction flow sheets originally supplied by Chinese engineering teams

Use of Chinese‑manufactured extraction equipment, mixers, settlers, and control systems

On‑site commissioning and troubleshooting by Chinese technical personnel

Supply of Chinese‑origin reagents or intermediate products used in purification steps

Each of these touchpoints can now intersect with technology export controls, particularly where process documentation, digital plant twins, or remote monitoring would be transmitted across borders. The message encoded in the regulations is clear: replicating Chinese‑grade separation performance abroad using Chinese technology is no longer a purely commercial matter; it is a licensable strategic transfer.

3. Downstream Magnets, Catalysts, and Batteries

Downstream, the most visible impacts concentrate in permanent magnets (NdFeB, SmCo), catalysts, phosphors, and battery materials. The inclusion of neodymium, dysprosium, terbium, samarium, and praseodymium in references to controls effective from 1 December 2025 [4] directly intersects with:

Traction motors in electric vehicles

Direct‑drive generators in offshore and onshore wind turbines

High‑performance robotics and industrial drives

Precision guidance, radar, and other defence‑related systems

For lithium‑ion batteries and artificial graphite anodes, the controls touch a different but closely related set of operations: anode material manufacturing, coating, and cell assembly. The net effect is a tighter alignment of rare earth and battery value chains under a single export‑control umbrella, particularly for systems where REE‑based motors and high‑performance battery chemistries co‑exist.

4. European Exposure and Structural Vulnerabilities

European institutions have highlighted that the REE export controls adversely affect industries central to the EU’s digital, green, and defence strategies [7]. Despite the partial suspension, the measures exposed structural vulnerabilities: limited domestic separation capacity, slow permitting for new processing plants, and high dependence on Chinese magnets and battery materials.

The critical insight from the European perspective is that diversification at the ore stage is insufficient if midstream refining and magnet production dependencies remain concentrated. Export controls that sit at these midstream nodes can disrupt European manufacturing even when mines are located on other continents.

VI. Compliance Risk as Industrial and ESG Risk

1. From Legal Exposure to Operational Disruption

For companies embedded in REE‑intensive supply chains, export control compliance is not only a legal concern; it is an operational continuity issue. Shipments held for licensing review, revoked authorisations, or retrospective questions about origin can halt production lines that rely on just‑in‑time deliveries of magnets, oxides, or battery components.

Misalignment between procurement, engineering, and compliance teams can introduce additional risk. Engineering decisions that substitute one magnet grade for another, or that adjust alloy formulations, may change the controlled content profile of a product without immediate visibility at the compliance level. The 0.1% rule makes such shifts material from a regulatory standpoint even when they appear marginal in cost or performance terms.

2. Environmental and Social Constraints on Alternative Supply

Building alternative supply chains outside China is not frictionless. Rare earth separation and magnet manufacturing carry significant environmental footprints: radioactive waste handling, acid consumption, wastewater treatment, and energy‑intensive calcination and reduction steps. In many jurisdictions, ESG and permitting frameworks impose longer lead times and stricter operating conditions on such facilities than in incumbent Chinese hubs.

As a result, any accelerated push to re‑shore or friend‑shore REE processing into Europe, North America, or allied states intersects with local community acceptance, tailings management constraints, and capital‑intensive environmental controls. Export controls thus do not simply redirect flows; they interact with domestic ESG frameworks to shape which projects can realistically move from plan to operation within the 2025–2028 horizon.

3. Industrial Resilience and Continuity Planning

Within this context, industrial resilience strategies observed across sectors have tended to combine multiple elements: diversifying supplier bases where technically feasible, adjusting specifications to accommodate alternative magnet or alloy grades, and in some cases revisiting inventory policies for key REE‑intensive components.

In heavy industry and defence‑related applications, several actors have explored onshore or near‑shore processing routes, often in partnership with technology providers from Japan, Europe, or North America that offer non‑Chinese process designs. These efforts remain constrained by lead times, permitting, and the need to reach competitive recovery rates and purity specifications (for example, TREO purity thresholds or ppm impurity limits in high‑coercivity magnets), all under ESG and cost pressure. Export controls tilt the trade‑off: industrial continuity increasingly depends on the ability to operate within, or partially outside, the evolving Chinese licensing perimeter.

VII. November 2026 Scenario Space: Reactivation, Suspension, Recalibration

The temporary suspension of the second wave until 10 November 2026 creates a defined decision point in the regulatory horizon. Public sources and expert commentary outline several plausible trajectories, each with distinct technical and operational consequences.

1. Scenario 1 – Full Reactivation on 10 November 2026

In a deterioration of trade negotiations or escalation of geopolitical tensions, Beijing could allow the suspension to lapse and activate the second wave essentially as written. In that scenario, the 0.1% extraterritorial rule and the full suite of technology controls would apply from late 2026 onwards, with licensing risk extending deeply into foreign manufacturing.

Earlier scenario analysis referenced in the original French assessment suggested that, under such a full reactivation, prices for permanent magnets and rare earth components could plausibly rise in the order of 15–30% due to compliance frictions and constrained supply. Such figures are indicative rather than deterministic, but they illustrate the way administrative bottlenecks can translate into cost structures, particularly if licensing queues lengthen and high‑risk destinations face systematic denials.

From a technical operations perspective, this scenario would re‑elevate the importance of precise origin tracing and product redesign capabilities. Plants relying on Chinese technology support might confront sharper constraints on software updates, remote diagnostics, or process optimisation assistance, especially where exports feed sensitive end uses.

2. Scenario 2 – Extended Suspension with Targeted Adjustments

A second trajectory envisaged in policy discussions is extension of the suspension beyond November 2026, accompanied by adjustments to fine‑tune scope. Adjustments could, for example, recalibrate the de minimis threshold, refine the list of controlled end uses, or narrow technology categories where enforcement has proven administratively challenging.

In this scenario, the architecture of extraterritorial control remains on the books but is applied in a more selective manner. Compliance systems built during 2025–2026 remain necessary, yet day‑to‑day disruptions are moderated. Strategic leverage is preserved, while some of the highest‑friction aspects are dialled back to reduce collateral impact on industries not central to the security narrative.

A third plausible path combines partial reactivation with sharper sectoral focus. Under this approach, full 0.1% extraterritoriality and stringent technology controls could be applied to a narrow band of applications—such as advanced defence systems, high‑end lithography, or specific categories of EV and grid equipment—while other sectors experience looser application or streamlined licensing.

For industrial actors, this would differentiate risk profiles by end market rather than by material alone. Magnet producers serving consumer appliances might operate under relatively stable licensing regimes, while those supplying aerospace or radar systems could see heightened scrutiny. The same material—say, a dysprosium‑enriched NdFeB magnet grade—could therefore exist in parallel regulatory universes depending on its integration path.

VIII. Synthesis: Trade‑Offs, Structural Shifts, and Signals to Monitor

Across these waves of regulation, one pattern stands out: the centre of gravity has moved from bulk material exports toward control over process knowledge, equipment, and the cumulative presence of Chinese content in foreign products. This is not a simple matter of limiting tonnes of TREO crossing a border; it is a re‑engineering of who can build and operate high‑spec rare earth and battery material value chains, and under which jurisdictional constraints.

Several trade‑offs are becoming structurally visible. Re‑routing supply to non‑Chinese refiners trades off immediate availability against higher capex per MT of capacity and often higher opex linked to environmental compliance. Reliance on Chinese technology support for ex‑China plants preserves efficiency and yield but embeds exposure to technology export controls. Designing products to minimise controlled REE content can reduce licensing touchpoints but may introduce efficiency penalties or new dependencies on other controlled materials, such as specific battery chemistries or graphite grades.

After careful observation of early implementation, one key insight emerges: these controls are not simply another set of export licences; they alter the shape of engineering and procurement decisions. Choices about magnet composition, motor topology, or recycling routes are now inseparable from compliance architecture. The regimes around 0.1% thresholds and notification chains effectively convert technical design parameters into regulatory risk variables.

Signals that will matter most over the 2025–2026 window include the treatment of specific licence applications for dual‑use products, the practical enforcement intensity of Notification of Compliance requirements in multi‑tier supply chains, and the pace at which non‑Chinese separation and magnet capacities achieve stable operation under stringent ESG regimes. These signals collectively determine whether the November 2026 decision point crystallises into full reactivation, protracted suspension, or a calibrated middle path.

In this landscape, technical intelligence on process capabilities, material substitution pathways, and regulatory enforcement patterns becomes as critical as market pricing data. The rare earth sector has shifted into a mode where jurisdiction, technology, and traceability are co‑equal constraints on industrial planning, all under close surveillance active des signaux faibles.

Note sur la méthodologie TI22 TI22 Strategies integrates continuous monitoring of official texts (including MOFCOM announcements and customs notices), sectoral production and trade data, and technical specifications from end‑use applications. This triangulation enables alignment of regulatory language with actual process flows in mining, separation, and advanced manufacturing, highlighting where legal provisions intersect with real‑world operational bottlenecks.

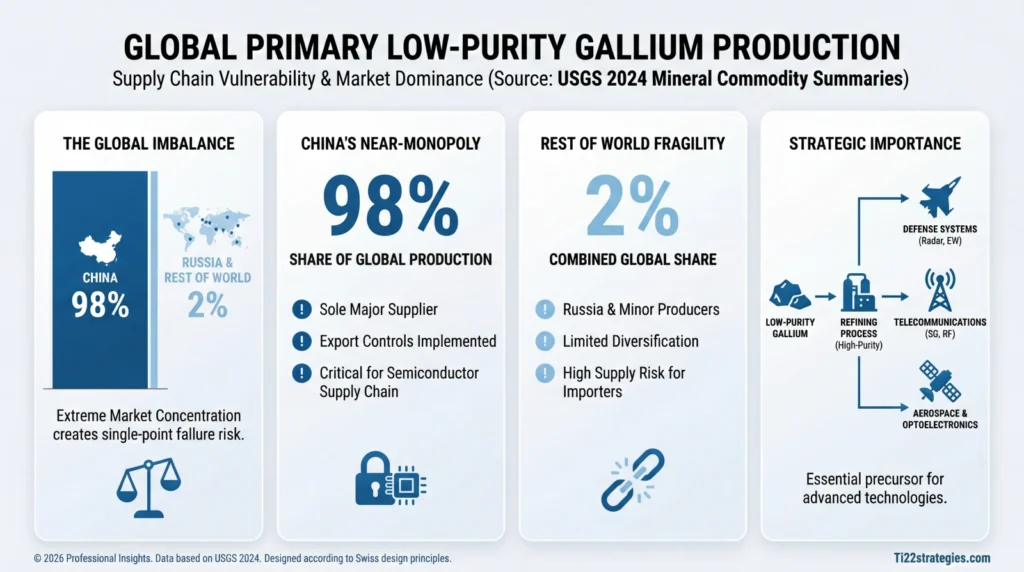

Executive Summary. The Chinese export control regime for gallium (Ga) and germanium (Ge) no longer operates as a hard stop on flows but as an adjustable-intensity mechanism, centered on three levers: (1) the granularity of material specifications and purity thresholds, (2) the classification of end-uses and end-users, and (3) an extraterritorial component based on MOFCOM Announcement 61. Since November 2025, a partial suspension, valid until November 27, 2026, has reopened access to standard licensing channels for U.S. civilian customers, while leaving military red lines intact. In practice, the dynamic is not defined by access to Ga-Ge volumes, but by licensing lead times, cascading traceability, supply chain fragmentation, and regulatory vulnerability looking toward late 2026.

The most structural feature of the system lies in the coexistence of suspensions with distinct timelines: one for restrictions specifically targeting the U.S. on Ga/Ge, and another for announcements extending the extraterritorial scope to products manufactured outside China. This dissociation creates a fragmented compliance window, where flows may appear regularized in the short term while remaining exposed to a regime shift in the medium term. The result is not merely legal; it translates into concrete industrial choices regarding refining localization, supplier qualification, and the configuration of multi-source logistics chains.

I. Control Regime Architecture: Material Scope and Technical Thresholds

A. Controlled Materials and Product Forms

The Chinese framework does not target gallium and germanium as abstract categories, but rather specific product forms and precise purity levels, articulated around strategic uses in optoelectronics and semiconductors. The control texts distinguish between raw metals, value chain intermediates (ingots, powders, compounds), and highly processed forms such as epitaxial wafers. This product-form approach allows for refined licensing selectivity, modulating severity between flows with potential military impact and those oriented toward mass civilian usage.

Gallium. Controls specifically cover pure gallium metal, gallium wafers used in the manufacture of high-frequency devices, and structural compounds such as gallium arsenide (GaAs) and gallium nitride (GaN) [2][6]. These forms are at the heart of 5G, RF power, LED, and advanced photovoltaic value chains. The control texts explicitly cover critical civilian applications, meaning the boundary does not lie between civilian and military, but within civilian segments themselves, depending on the end-user profile.

For gallium, the extraterritorial component is not limited to direct exports from China. It extends to products processed outside China that incorporate Chinese-origin gallium inputs, with no specific de minimis threshold declared for gallium alone, whereas a 0.1% de minimis rule applies to other categories of controlled materials [1][3]. This absence of an explicit threshold for Ga reinforces the potential scope of controls once Announcement 61 is fully in force.

Germanium. Germanium is treated similarly, but with particular emphasis on forms used in optics and infrared detection: raw germanium, ingots, powders, as well as compounds such as germanium dioxide dedicated to optical fibers [6]. These materials supply civilian segments (long-haul optical fibers, infrared optics for industrial imaging) and dual-use segments (defense optronics, night vision systems, guidance). Extraterritorial controls mirror those of gallium: any product manufactured outside China incorporating Chinese-origin germanium inputs or technologies may fall under the scope of MOFCOM licenses [3][5].

A key point for industrial directors is that the material does not cease to be controlled when it changes form: a flow of primary gallium melted into an ingot in a third country and then re-cut into wafers potentially retains the regulatory marking of its Chinese origin. Upstream traceability thus becomes a parameter as critical as purity or electrical characteristics in supplier qualification.

B. End-Use and End-User Rules

Beyond material specifications, the Chinese regime structures a hierarchy of permissiveness based on the end-user profile and the declared usage scenario [1][3]. The architecture of the texts converges toward a logic of structural denial for certain profiles, in-depth filtering for others, and standard treatment for a final circle.

Prohibited End-Users. Foreign military users are targeted for refusal in principle, as are entities listed on China’s export control list or watch list, including their subsidiaries, branches, or entities owned at least 50% [1]. In these cases, the logic is not to examine the transaction on a case-by-case basis, but to structurally block access to Chinese-origin Ga/Ge.

Prohibited End-Uses. The regime also prohibits the supply of Ga/Ge for the design, development, production, or use of weapons of mass destruction and their delivery systems [1], as well as for potential military applications, notably advanced semiconductors capable of powering defense systems [5]. This prohibition field functions as a functional filter: even a civilian user may be refused if the projected use falls into these categories.

U.S. Civilian End-Users. Since November 2025, the mechanism has evolved for this category: U.S. civilian customers once again have access to standard licensing channels [2][3][6]. This means their applications are no longer blocked by a principle-based ban, but processed under the ordinary framework, with evaluation of the dossier, end-use declarations, and user profile. Approvals remain discretionary, however, and the exact criteria for acceptance or refusal are not fully public.

The fundamental pivot lies in the shift from a presumed ban to licensing filtration. In industrial terms, the difference translates not only into the possibility of continuing supply, but into a new category of risks: delays, calendar unpredictability, and the possibility of sudden tightening of license processing without any apparent change in physical volumes available.

C. Extraterritorial Obligations and De Minimis Rules

MOFCOM Announcement 61 introduces an extraterritorial component that constitutes the most structural dimension for Ga-Ge value chains located outside China. It subjects products manufactured in third countries to licensing if they incorporate specified Chinese inputs or technologies, even if the final exporter is not established in China [3][5].

The text covers, notably, rare earth and strategic metal products manufactured outside China when they rely on Chinese technologies in five key steps [5]:

Mining extraction;

Smelting and separation;

Metal smelting;

Magnet or functional intermediate manufacturing;

Recycling and recovery of secondary resources.

For gallium and germanium, this logic extends to material flows: a Ga/Ge product manufactured outside China, but containing Chinese-origin inputs, may enter the scope of licenses, with no de minimis threshold explicitly fixed for these two metals [5]. The absence of a quantified threshold intentionally leaves a wide margin of appreciation to the control authority, complicating ex-ante regulatory risk modeling by product or client.

Current Status. As of January 2026, Announcement 61 is suspended until November 10, 2026 [2][3]. Concretely, the extraterritorial obligations it foresees are not applied during this period. However, this suspension does not represent a repeal: the legal framework remains in place and can be reinstated at the end of the suspension period without building a new architecture. For industrialists, this translates into an intermediate environment: part of Ga-Ge flows remains outside the effective scope, but under a latent regulatory threat less than twelve months away.

II. Implementation Schedule and Strategic Suspensions

A. Chronology of Announcements and Suspensions

Since the autumn of 2025, the regulatory trajectory has been organized in short sequences, with structuring announcements followed by partial suspensions. The following table summarizes the major milestones communicated in the cited sources:

Date

Announcement

Content

Current Status

October 9, 2025

Announcements 55, 58, 61, 62

Extended controls on rare earths, advanced semiconductors, processing technologies

Suspended until November 10, 2026 [2][3]

October 30, 2025

Pre-suspension

MOFCOM suspends implementation of October 9 measures for one year

In effect [7]

November 5, 2025

Announcement 72 (Partial)

Suspension of U.S.-specific restrictions on gallium, germanium, antimony, and super-hard materials

In effect until November 27, 2026 [3][6]

November 9, 2025

Announcement 72 (Full)

Suspension of Article 2 of Announcement 46 (2024), restoring standard licensing channels for U.S. civilian customers

In effect until November 27, 2026 [3][6]

Two dates emerge as distinct pivots for the operational management of Ga-Ge flows:

November 27, 2026: End of the suspension of restrictions specifically targeting gallium and germanium flows to the United States (possible reactivation of Announcement 46 effects for U.S. civilian customers) [6];

November 10, 2026: End of the suspension of Announcements 55, 58, 61, 62, which would pave the way for full activation of extraterritorial obligations [2][3].

This temporal asymmetry creates a period of approximately ten months where the dominant question is not the physical availability of Ga/Ge, but the anticipated trajectory of controls and the capacity of supply chains to absorb a potential regulatory regime change without operational rupture.

B. From Ban Regime to Standard Licensing Regime

Before November 2025, Announcement 46 (2024) instituted a principle-based ban striking re-exports of gallium and germanium to U.S. civilian customers [2]. The filter was then binary: flows authorized to certain countries and segments, flows structurally blocked to others. The sequence opened by Announcement 72 substituted this logic of prohibition with a standard licensing regime, returning to ordinary examination channels for U.S. civilian users [3].

Operational Example. A German distributor re-exporting Chinese-origin gallium wafers to a civilian semiconductor manufacturer established in the United States was previously blocked by Clause 2 of Announcement 46. Since November 2025, the same operation is theoretically possible subject to obtaining a standard license, the outcome no longer being decided by an automatic ban but by the evaluation of the application by the Chinese authority [2].

This change does not eliminate risk; it modifies its form. The critical point becomes the management of license queues, calendar uncertainties, and potential selective hardening for certain categories of users or uses. The architecture allows the Chinese regulator to adjust pressure on Ga-Ge flows at a much finer rhythm than a frontal ban permitted.

III. Operational Implications: Supply Chain Friction and Compliance Burdens

A. Lengthening Lead Times and Regulatory Uncertainty

Licenses are becoming the new operational unit of measurement for Chinese-origin Ga-Ge flows. Available sources do not precisely document average lead times for licenses targeting gallium and germanium. Nevertheless, the general Chinese regime for dual-use goods mentions review ranges on the order of several weeks, which can extend when the end-user or end-use justifies reinforced examination [4].

Added to this temporal layer is the uncertainty linked to suspensions: the environment of January 2026 relies on transitional regimes expiring in November 2026. Chinese authorities insist in their communications on the legal and non-discretionary nature of export controls, while retaining the possibility of reactivating stricter measures at the end of suspensions [6]. For value chains, the direct consequence is the multiplication of scenarios to manage in parallel: continuity of the standard licensing regime, return to a more restrictive regime, or full activation of extraterritorial mechanisms.

B. Civil/Military Segmentation and End-User Verification

The Ga-Ge regime relies on strict segmentation between civilian and military supply chains, which reverberates down to intermediate distribution levels [1][3]. This segmentation is not merely a contract clause; it implies evidentiary mechanisms and technical filtering tools.